Understanding Medical Bills

Medical billing in the United States can seem like an extremely convoluted process. According to a 2016 public opinion survey conducted by Copatient, around 72% of American consumers are confused by their medical bills, and 94% of consumers have received medical bills they considered to be “too expensive”. Even when covered by insurance or Medicare, you may find unexpected balances due to odd procedural codes, a slew of medical jargon, and insurance adjustments.

This guide will help you, as a patient, navigate the medical billing process from the moment you contact a healthcare provider about an appointment until after you receive your bill in the mail. We discuss how healthcare providers determine costs and negotiate charges with your insurance provider. Finally, we show you how to identify and dispute erroneous charges on your bill.

What Medical Bills Really Cover

Fees might seem arbitrary when you ask for cost estimates from your insurer or when you receive a bill after your appointment. However, there are several elements that factor into how hospitals, physicians’ offices, and other institutions calculate the cost of health services. If possible, contact your insurer to get cost estimates for multiple healthcare providers in your area. You may discover fees vary quite a bit for the same services.

In a New York Times op-ed entitled “Why Medical Bills Are a Mystery,” professors Robert Kaplan and Michael Porter of Harvard Business School explain that providers “assign costs to patients based on what they charge, not on the actual costs of the resources, like personnel and equipment used to care for the patient.” Here are the considerations medical offices and hospitals make as they negotiate with insurance companies about the costs that appear on your bill:

- Facility capacity: Hospital capacity growth is a factor that the National Institute for Health Care Management (NIHCM) Foundation watches closely, since the number of beds in a hospital can dramatically influence what hospitals charge under a fee-for-service (FFS) system. As hospitals add more beds, they have a greater opportunity to provide certain medical services. As the NIHCM notes, “Higher system capacity can lead to competition among suppliers and downward pressure on prices.”

- Supply and demand: How readily available are the services you need? Are there multiple high capacity hospitals or physicians’ offices in your area that can provide this service, or do you just have access to a limited number of specialists? Dr. Robert Stonebraker explains in his open source book, The Joy of Economics, “Firms facing little or no competitive pressure are free to raise prices well above the true cost of service. Monopoly power drives up prices in medical care, just as it would it in retailing and restaurants.”

- Hospital reputation: A hospital’s reputation has a ripple effect on how many patients use a facility, which in turn influences demand and cost. However, the Agency for Healthcare Research and Quality warns consumers that “Clinical quality scores contributed little to hospital choice compared with a hospital’s reputation.” This can drive business and influence service costs, but you shouldn’t rely on perceived reputation as an indication of performance and quality.

- Charge Description Master (CDM) lists: This resource is a master list of service costs and billing identifier codes that medical billing professionals use during the claims process as health offices calculate how much to bill insurance companies and patients. Each hospital maintains its own individual chargemaster list. The American Health Information Management Association (AHIMA) recommends that CDM prices should be maintained by chargemaster committees that oversee responsibilities like “reviewing all charge dollar amounts for appropriateness by payer.”

Medical billing and coding professionals are working behind the scenes from the moment you schedule an appointment up until you receive a bill. Most patients aren’t familiar with the negotiations that occur between insurance companies and healthcare providers. Understanding the back and forth can take some of the mystery out of the insurance and billing processes.

How the Billing Cycle Works

- You contact a healthcare provider. Pre-register and provide basic information to the office, such as identification and insurance information. You schedule an appointment.

- It is important to ask the healthcare provider about the services and supplies you’ll receive. If you are not clear on upcoming charges or what insurance will cover for the appointment, then be sure to ask for the procedure codes.

- Next, contact your insurance company to find out if these services are covered by your plan. If so, get an estimate of how much the services cost with your health insurance.

- If the cost is not manageable, ask your insurer if there are other healthcare providers in your area who provide the same service for less.

- The healthcare provider contacts your insurance company in order to verify:

- Preauthorization: Some insurance companies require prior authorization before they cover a medical service or medication. The insurance company collects further information regarding your appointment and medical records before determining whether the services and medications are covered.

- Co-Pay: The healthcare provider’s office also determines how much the patient must pay out-of-pocket for this visit.

- On the day of the appointment, you complete any additional registration paperwork, supplying your insurance card, a valid ID, policyholder name, and your insurance group number. This registration process helps healthcare providers:

- Update your medical records electronically; pre-existing conditions can factor into coverage decisions

- Provide you with privacy policy information

- Gain your consent to perform certain procedures

- Inform you of care liability and risks

- Inform you of patient financial responsibilities

- Determine your advanced directive preferences, which will give healthcare providers clear instructions if you are unable to speak for yourself

- After services are received medical coders identify all services, prescriptions, and supplies received during your appointment and update your records with the corresponding service codes.

- The healthcare provider creates an insurance claim using these codes. They then submit an 837 file to your insurance, the standard file format set by the Health Insurance Portability and Accountability Act (HIPAA), allowing your healthcare provider to communicate securely with your insurance.

- A claims processor, who works for your insurance provider, reviews the insurance claim and verifies that the treatments you’ve received fall under your coverage benefits. (At this point, the insurance claims processor may contact you or your healthcare provider for additional information regarding the services and/or supplies you received.) The insurance claims processor decides whether the claim is valid, and then accepts or rejects it.

- The insurance claims processor contacts your healthcare provider with the status decision. If the claim is valid, insurance reimburses your healthcare provider by paying for some or all of the services. If rejected, the claims processor provides the billing office with a detailed description of why the services are not covered.

- Your healthcare provider bills you for the remaining balance.

NOTE: If you are 65 or older, you are entitled to federal health benefits through Medicare. This social insurance program differs significantly from private health insurance providers when it comes to billing. Rather than negotiating prices with a healthcare provider like private health insurers, Medicare publishes set fees for services. If you are enrolled in Medicare Part B, your healthcare provider consults the Medicare Physician Fee Schedule (MPFS) to determine the set price for the services you received.

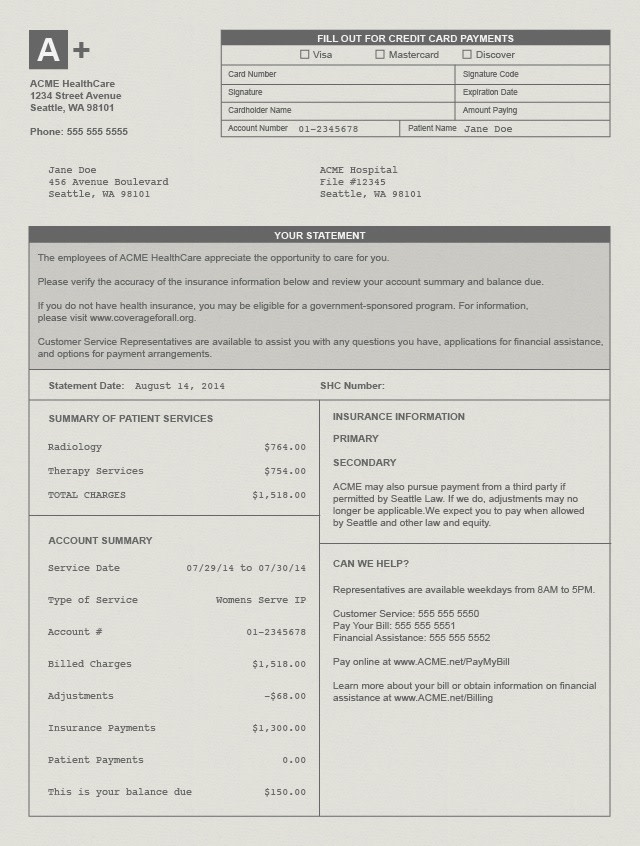

How to Read Your Bill

Once you receive a medical bill from your healthcare provider, you will notice that it consists of multiple components that might not be clear to you. For most patients, the codes, descriptions, and prices listed in their bills can seem confusing.

The following example explains each element of your bill with an in-depth description. It is important not to get your medical bill confused with the Explanation of Benefits (EOB), an insurance report we cover following the bill.

- Statement Date: The date your healthcare provider printed the bill.

- Account Number: This is your own unique account number. If you have questions regarding your bills and balance, you need to provide this number when contacting your healthcare provider’s billing office. Account numbers are also typically used when you pay for a bill online.

- Service Date: Your bill includes a column listing the dates you received each medical service.

- Description: This is a short phrase that explains the service or supplies you received.

- Charges: This is the full price of the services or supplies you received before insurance has been factored in.

- Billed Charges: This is the total amount charged directly to either you or your insurance provider.

- Adjustment: This is the amount the healthcare provider has agreed not to charge.

- Insurance Payments: The amount your health insurance provider has already paid.

- Patient Payments: The amount you are responsible to pay.

- Balance/ Amount Due: The amount currently owed the healthcare provider.

- Payable to: This is the organization you should address check payments to.

You may also see a “service code” listed on your bill. Healthcare providers use a standardized Current Procedural Terminology (CPT) or Healthcare Common Procedure Coding System (HCPCS) to identify the exact services and supplies you received during your appointment. NOTE: Coding protocol is used internally and may not be included on your bill.

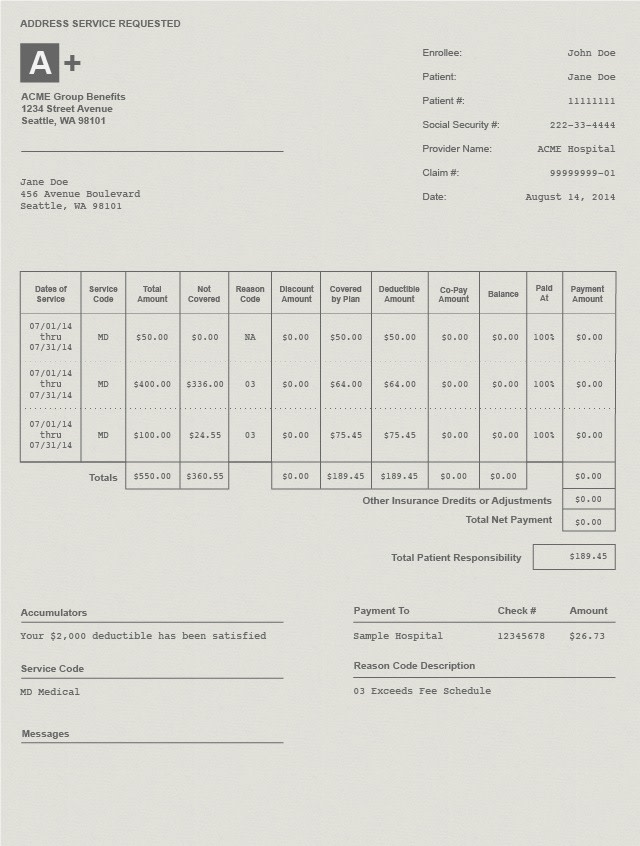

What is an Explanation of Benefits (EOB)?

An EOB is a document sent to insured individuals after a claim has been submitted by a healthcare provider. It explains what medical treatments and services the patient’s health insurance company agreed to pay for and what treatments/services (if any) the patient is responsible for paying. EOB stands for explanation of benefits. It is not the same as a medical bill, although it may look similar and show a balance due. When the EOB indicates that money is still owed to the doctor or dentist who provided care, patients can expect a separate bill to be sent from the doctor or dentist’s office. In this instance, payment should be made directly to the practitioner, not to the insurance company who sent the EOB. The purpose of EOBs is to keep consumers informed of their healthcare costs and expenditures. It also offers insured customers a chance to double-check that services are billed correctly.

- Member Information: This shows the health insurance member’s full name and ID number.

- Patient Account Number: This is the unique identification number used by your healthcare provider to track your account.

- Provider Name: The name of the hospital, physicians’ office, or healthcare professional you visited during your appointment.

- Claim Number: This unique identification number is used by your insurance provider to track your account.

- Date of service: The date you received the medical services, procedures, or supplies.

- Service Code: This identifies the specific services, procedures, or supplies you received from a healthcare provider.

- Total Amount: This dollar amount shows the full cost of the procedures, services, or supplies.

- Not Covered: This is the amount your health insurance does not cover. You are responsible for this amount.

- Reason Code Description: This code provides the reason(s) why your insurer did not cover a charge.

- Covered by Plan: This is the total amount your health insurance provider has saved you.

- Deductibles and Copayments: Adjustments added based on the deductible and copay features of your insurance plan.

- Total Net Payment: This includes the full dollar amount your insurance company has paid to your healthcare provider.

- Total Patient Responsibility: This is the total amount you owe your healthcare provider.

- Checks Issued: This section gives you a detailed record of the payment transactions from your insurer to your healthcare provider. These lists generally contain the payee’s name, check number, and check amount.

Dealing With Billing Errors

Since medical billing processes involve several parties – you, your insurer, and your healthcare provider – mistakes can and do happen. A medical coder might have inaccurately described your care history with an inaccurate code, a medical biller might have mistyped a value, or a claims adjuster might have applied the wrong plan information to your claim. Regardless of the reason behind this error, it is important for you as a patient to monitor your bills and EOB forms. If you notice charges that look out of place, do not hesitate to contact your insurers and/or healthcare providers to dispute the error.

Identifying Errors

- Compare estimates to your final bill: Before your appointment, contact the healthcare provider and ask to be given the billing code and cost. Next, contact your health insurance provider to make sure the procedure is covered by your plan and obtain an estimate of how much you will need to pay for the procedure. If your estimated total is very different from your balance due after the appointment, there may be a billing error.

- Create a list of charges: Create a record of all the medical services and supplies you received, along with their corresponding charges. This can help you identify an incorrect charge in the future.

- Duplicate charges: If you notice the same charge listed twice, it is likely that an error occurred during data entry.

- Beware of upcoding: Upcoding is the criminal act of fraudulently reporting an incorrect diagnosis in order to profit. A disreputable healthcare provider might use upcoding so it receives a large payment from you or your insurance company. If a procedure description or code seems to include services you did not agree to, it could be a form of upcoding.

- Check identifying information: Make sure your name and identification numbers are correct. Mistakes in identification could lead to insurance coverage discrepancies.

Disputing Charges

- Contact your healthcare provider’s billing office: Speak to your healthcare provider about bill inaccuracies. If they made an error during the claims process, they should be able to correct it. Take note of the billing representative, the date, and time of your phone call.

- Call your insurer: If you are unable to resolve the error with your healthcare provider, contact your insurer about the disputed charge. They can work with you to file a formal appeal to dispute a charge. They can also examine your bill for red flags that could indicate fraudulent activity committed by the healthcare provider.

- Contact a credit-reporting agency: Make sure your disputed bills do not impact your credit score. As you dispute a charge, your healthcare provider might mark the bill as overdue, which can impact your credit score. Your credit agency should be able to address credit score issues if you are still disputing a charge.

- Credit reporting agencies:

- Experian

- TransUnion

- Equifax

Above all, remember to not be afraid to ask questions when at the hospital or doctor’s office; it is important to properly grasp what is covered by your insurance. Maintain a record of your medical bills and keep an eye out for errors and discrepancies.

Unlock a career in medical billing and coding and make a difference in the healthcare industry.

Discover schools with specialized programs that empower you to make a difference today.

Learn More About Our Partners

© 2023 MedicalBillingandCoding.org , a Red Ventures Company

Advertising Disclosure Cookie Settings

- About

- Contact

- Privacy Policy

- Do Not Sell or Share My Personal Information

- Terms of Service

- Consumer Health Data Privacy Policy